What Are the Different Types of Tokenized Stock?

An educational article based on the Tokenized Podcast, co-hosted by Simon Taylor and Cuy Sheffield, drawing on a framework developed by securities researcher Borja Neira.

Not All Tokenized Stocks Are Created Equal

Tokenized equities are having a moment. Every week brings fresh headlines — the New York Stock Exchange announcing plans to tokenize stocks for 24/7 trading, DTCC exploring blockchain-based settlement, NASDAQ piloting digital asset infrastructure, and Robinhood launching stock tokens for European users. The largest institutions in traditional finance are placing enormous bets on bringing equities onchain.

But beneath the surface-level excitement, there's a critical nuance that most coverage misses: the term “tokenized stock” covers wildly different structures with wildly different risk profiles. Buying a “tokenized stock” from one platform might mean you hold a direct, registered ownership stake in a company. Buying one from another platform might mean you hold a derivative contract with no legal claim to the underlying shares whatsoever.

The distinction matters enormously — for your rights as an investor, for counterparty risk, and for what happens when things go wrong.

“Every week there is a new major announcement around something related to tokenized equities. You have DTCC, you've got NASDAQ, you've got New York Stock Exchange. Every major player in traditional securities is clearly making big bets. I still haven't wrapped my head around what are the differences between all these approaches.”

— Cuy Sheffield, Head of Crypto at Visa

Sheffield's honest observation captures the challenge facing everyone in this space. The vocabulary is the same — “tokenized stocks,” “stock tokens,” “onchain equities” — but the underlying mechanics are radically different. Without a clear framework for understanding these differences, investors risk making uninformed decisions about what they actually own.

The Four Types of Tokenized Stock

Borja Neira, a securities and blockchain researcher, developed a framework that categorizes tokenized equities into four distinct types — labeled Type A through Type D. It has become one of the most useful lenses for understanding the tokenized stock market.

The framework is elegant in its simplicity: as you move from Type A to Type D, you get progressively more intermediary risk and progressively fewer ownership rights. At one end, you hold direct, registered ownership of the underlying stock. At the other end, you hold nothing more than a derivative contract — a promise from a counterparty that tracks the stock's price.

Understanding where a particular product falls on this spectrum is essential for any investor considering tokenized equities.

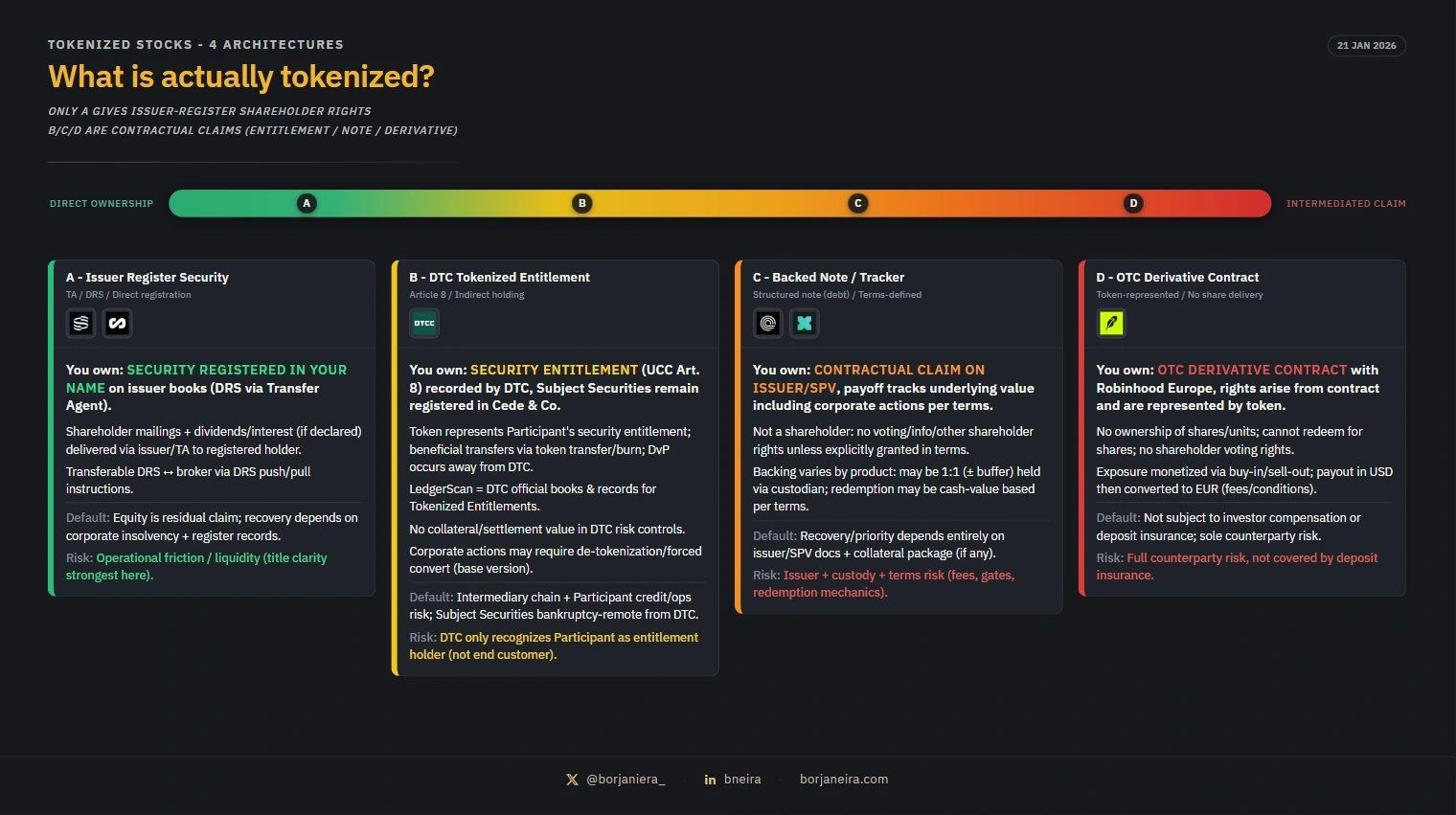

Type A: Issuer-Register Securities

Type A represents the gold standard of tokenized stock ownership. In this model, the company itself issues shares directly on a blockchain. Your name appears on the company's share register. The token you hold is the stock certificate — not a representation of it, not a claim on it, but the actual legal instrument of ownership.

“At the most extreme ownership end is what Superstate does and what Figure are doing with Open. This is where holding the token is direct ownership of the stock certificate. It would be like holding the physical stock certificate.”

— Simon Taylor, Author at Fintech Brain Food

With Type A tokenization, you have full shareholder rights. You can vote on corporate actions. You receive dividends directly. You have standing in the event of bankruptcy or litigation. There are no intermediaries between you and your ownership stake — the blockchain serves as the authoritative record of who owns what.

Companies like Superstate and Figure's Open network are pioneering this approach. Superstate, for example, is building infrastructure that allows fund shares to exist natively onchain, with the token itself serving as the legal record of ownership. Figure's Open network takes a similar approach, using blockchain as the primary registry for securities.

The trade-off is availability. Because the company itself must choose to issue shares in this format, Type A tokenized stocks are limited to issuers that have opted into blockchain-based registries. You can't retroactively tokenize Apple or Tesla shares as Type A — the issuer has to participate. This means the universe of Type A tokenized securities is currently small, though growing as more companies and funds recognize the efficiency gains of onchain issuance.

Type B: DTC-Tokenized Entitlements

Type B mirrors the structure of a traditional brokerage account, but uses blockchain as the settlement and record-keeping layer. In this model, the actual shares are held by the Depository Trust Company (DTC), specifically by its nominee Cede & Co, which is the registered owner of the vast majority of publicly traded securities in the United States.

When you hold a Type B tokenized stock, you have the economic rights and obligations associated with the shares — dividends, voting rights (passed through to you by your broker), and the ability to sell — but you don't have direct custody of the stock certificate. Instead, you hold a tokenized entitlement that represents your beneficial ownership interest in shares held at the DTC level.

This is what the New York Stock Exchange is building toward. Their announced initiative to tokenize stocks for 24/7 trading would likely create tokenized representations of shares that remain in the existing DTC infrastructure. The blockchain layer adds programmability, extended trading hours, and potentially faster settlement, but the underlying custody arrangement mirrors the system that already powers most of the stock market.

The advantages of Type B are significant: it can cover the entire universe of publicly traded securities without requiring issuer participation. Any stock held at the DTC could theoretically be tokenized in this way. The structure is familiar to regulators, and the legal framework for beneficial ownership through DTC is well-established.

The limitations are also real. Fractionalization is more complex because the underlying shares at DTC are whole units. The tokens don't float freely in DeFi markets the way a natively onchain asset would, because they're tethered to the DTC's centralized infrastructure. And there's an inherent reliance on the DTC and its participant brokers as intermediaries, which adds layers between the investor and the underlying asset.

Type C: Backed Notes and SPV Wrappers

With Type C, the nature of what you own changes . You do not own the stock. You own shares in a special purpose vehicle (SPV) — a fund or legal entity — that owns the underlying stock on your behalf. The token represents your interest in the SPV, not a direct claim on the equity.

This structure is common in private market secondary sales. When platforms offer tokens representing shares of pre-IPO companies like OpenAI, they typically use SPV wrappers. A fund acquires the shares, then issues tokens to investors representing their pro-rata interest in the fund. The investor gets economic exposure to the stock's price movement, but the legal relationship is between the investor and the SPV — not between the investor and the company whose stock the SPV holds.

“Are there real stocks that you are actually owning? Because what Robinhood did, if I'm not mistaken, is they did an SPV. So it's actually not the stock that you own when you own that stock. If you had a dividend associated with that stock, you have no guarantee that that dividend is coming to you.”

— Eric Piscini, CEO of Hashgraph

Piscini highlights the crucial distinction: with Type C, your rights are governed by the terms of the SPV, not by securities law as it applies to direct shareholders. Whether dividends pass through to you depends on the SPV's governing documents. Your ability to vote on corporate actions may be limited or nonexistent. And if the SPV operator goes bankrupt or acts improperly, your recourse is against the SPV — not against the company whose stock you thought you were buying.

The advantage of Type C is that it can provide exposure to assets that would otherwise be inaccessible — private company shares, foreign securities, or fractionalized positions in expensive stocks. The disadvantage is the additional layer of counterparty risk and the dilution of shareholder rights.

Type D: OTC Derivative Contracts

Type D is the furthest from actual stock ownership. In this model, there are no shares at all — no direct ownership, no SPV holding stock on your behalf, no entitlement to shares at a depository. What you hold is a derivative contract — an agreement with a counterparty that pays you (or charges you) based on the price movement of a stock.

“What Robinhood has done is really a derivative contract that is essentially buying you exposure to the price movement without actually you having any legal ownership whatsoever of the underlying stock.”

— Simon Taylor, Author at Fintech Brain Food

This is what Robinhood launched in the European Union — a perpetual future derivative that tracks the price of US stocks. Users get price exposure, but they don't own the stock. They don't receive dividends (unless the contract specifically provides for dividend-equivalent payments). They can't vote. They have no claim in a bankruptcy proceeding against the company.

The risk profile here is entirely about counterparty exposure. Your position is only as good as the platform's ability and willingness to honor the contract. If the platform becomes insolvent, you're an unsecured creditor — you don't hold any underlying asset that can be returned to you. This is a different risk profile from holding actual shares, even through a brokerage.

Type D products are common in crypto markets because they're relatively simple to create. A platform doesn't need to custody actual securities, manage transfer agent relationships, or comply with the full suite of securities regulations that apply to stock issuance. But the simplicity for the platform comes at a cost to the investor — less protection, fewer rights, and more counterparty risk.

Why the Distinction Matters

The differences between these four types become painfully clear in edge cases. Consider a corporate spin-off — when a company splits into two separate entities. If you hold Type A or Type B tokenized stock, you're a real equity holder: you receive shares in both the parent and the new company, just as any other shareholder would. But if you hold a Type C SPV wrapper or a Type D derivative contract, the platform may simply pay you “cash-in-lieu” — a cash settlement based on the estimated value of the new position, rather than actual shares in the spun-off entity.

The same issues arise with dividends, stock splits, rights offerings, tender offers, and merger considerations. Real shareholders have legal protections and established procedures for all of these events. Token holders at the Type C and Type D level are at the mercy of the platform's policies and the fine print of their agreements.

As you move from Type A to Type D, a clear pattern emerges: more intermediary risk and fewer ownership rights. Type A holders have the strongest legal position and the least counterparty exposure. Type D holders have the weakest legal position and the most counterparty exposure. Types B and C fall in between, with meaningful trade-offs at each level.

“It would be great to see some sort of regulation or guidance come out from a securities regulator to say, this is how you tokenize stocks.”

— Chris Harmse, Co-Founder of BVNK

Harmse's call for regulatory clarity reflects a growing consensus in the industry. Without clear standards, investors are left to decode legal documents and product disclosures to understand what they actually own — and many won't bother, assuming that “tokenized stock” means the same thing everywhere.

Where the Industry Is Heading

The good news is that the industry is not converging on a single model — it's building infrastructure that can support multiple approaches simultaneously. The NYSE's announcement signals support for institutional-grade tokenization at the Type B level. DTCC is actively exploring how its existing depository infrastructure can interface with blockchain networks. Meanwhile, issuers like Superstate and Figure are pushing forward with Type A direct issuance.

One of the most interesting developments is the potential for composability — the ability for tokenized stocks to interact with other onchain financial primitives like stablecoins, lending protocols, and decentralized exchanges. This is where the promise of tokenized equities extends far beyond just 24/7 trading.

“Part of the announcement that stood out to me was Vlad mentioned these stock tokens that in the future, you'll be able to withdraw them to your self-custodial wallet and then be able to use them connected to protocols and benefit from the composability.”

— Cuy Sheffield, Head of Crypto at Visa

Sheffield is referencing Robinhood CEO Vlad Tenev's comments about stock tokens eventually being withdrawable to self-custodial wallets. If realized, this would mean investors could take their tokenized stocks and use them as collateral in DeFi protocols, trade them on decentralized exchanges, or hold them in wallets they fully control — a radical departure from the traditional brokerage model where your broker holds everything for you.

The settlement implications are just as significant. When both stocks and stablecoins exist onchain, settlement can happen atomically and instantly. Instead of the traditional T+1 (or even T+2) settlement cycle, a trade could settle in seconds — the buyer's stablecoins and the seller's stock tokens swap simultaneously in a single transaction. No clearing house needed. No settlement risk. No failed trades.

Then there's the access question. Billions of people around the world cannot easily buy US equities due to regulatory barriers, high brokerage fees, and limited infrastructure. Tokenized stocks — particularly at the Type C and Type D level — could open access to global equity markets for investors in emerging economies who currently have no practical way to participate. While these structures carry more risk, they may be the only realistic path to democratizing equity ownership at a global scale.

And of course, 24/7 trading. Crypto markets never close. If stocks are represented as tokens, there's no technical reason they should only trade during US market hours. Weekend trading, overnight trading, and holiday trading all become possible — matching the always-on nature of global financial markets.

What This Means for Investors

If you're considering buying tokenized stocks, here's what you need to keep in mind:

- Understand what you actually own. Don't assume that “tokenized stock” means you own the stock. Read the fine print. Ask whether you hold a direct security, a beneficial entitlement, an SPV interest, or a derivative contract.

- Check the structure (A/B/C/D). Use the framework above to categorize any tokenized equity product before you invest. The type determines your rights, your risk exposure, and what happens in corporate events like dividends, spin-offs, and mergers.

- Consider counterparty risk. As you move from Type A toward Type D, your exposure to the platform or issuer increases. Ask yourself: if this platform shuts down tomorrow, what happens to my position? With Type A, your shares exist on a blockchain registry. With Type D, your position may simply vanish.

- Regulation is coming, but it's not here yet. Securities regulators are watching this space closely, but clear rules for tokenized equities are still being developed. Until regulatory frameworks catch up, investors bear additional risk from regulatory uncertainty — rules could change, platforms could be forced to restructure, and certain products could be banned in certain jurisdictions.

The tokenized stock market is one of the most exciting developments in capital markets in decades. The combination of 24/7 trading, instant settlement, global access, and DeFi composability could reshape how equities are issued, traded, and held. But the promise of that future depends on investors understanding the difference between owning a stock and owning a contract that tracks its price.

The framework is simple. The implications are profound. Know what you own.

This article is based on the Tokenized podcast episodes

This article is for informational purposes only and is not financial, business, or legal advice. Views and opinions are those of the contributors and do not represent the opinions of any company they represent. When you buy cryptoassets your capital is at risk. Please do your own research.

This article is part of the Tokenized learning series — educational content on stablecoins, tokenization, and real-world assets from the Tokenized podcast, hosted by Simon Taylor and Cuy Sheffield.